Our recent study of more than 60,000 campaigns across 20+ countries revealed that only around 53% of ad impressions served across Europe were delivered to the audience advertisers intended.

This high level of inaccuracy was particularly acute for campaigns targeting women, with only 46% of ad impressions meant for women being served to them, compared to 62% accuracy among men. Part of the reason it’s harder to accurately target women than men is that internet usage among men tends to be heavier, particularly younger men, so they’re generating more activity and, therefore, there are comparatively more opportunities to reach them.

So what do these benchmark scores mean for doing business and what are the key trends coming out of them?

Advertisers more keen on independent measurement

The first thing to point out is that the depth of data available has increased, with the number of campaigns measured across Europe through the Digital Ad Ratings (DAR) service more than doubling year-on-year. Furthermore, the proportion of campaigns involving a mobile element nearly tripled from 22% to 58%.

As the digital media ecosystem becomes more complex, this large rise is indicative of more marketers viewing independent measurement as vital in ensuring they’re actually reaching their audience and maximising ROI. This echoes the ongoing calls from the buying community for greater visibility about campaign performance from independent third parties.

Use audience benchmarks in your negotiations

The benchmarks provide a good snapshot of performance, but their usefulness is much wider. You should be using them to hold media owners to account and get them to improve. Where they fall below benchmarks, ask for discounts or ‘make goods’. Where they over-perform, reward them with more business and a greater share of your spend. We see the largest advertisers utilising the data this way to help strengthen their negotiating positions and, ultimately, move towards a buying approach more akin to TV.

Don’t get too hung up on the differences between advertising sectors

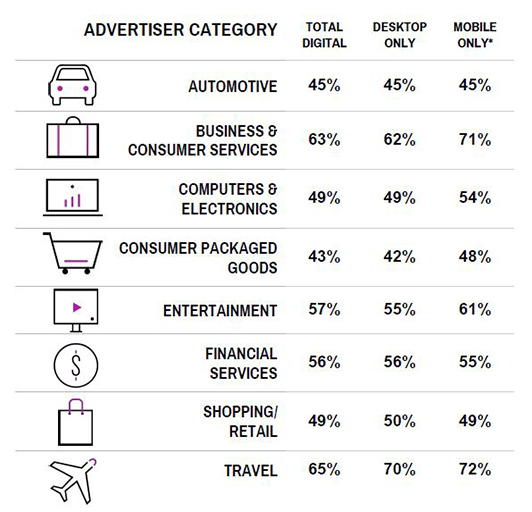

The data showed some interesting metrics about how accuracy differs across major advertising sectors. For instance, Travel marketers were the most likely to reach their desired audience (doing so 65% of the time) followed by Business/Consumer services (63%). In contrast, FMCG (43%) and automotive (45%) marketers struggled most to reach their target audience.

However, it’s wise to look beyond this and understand that this really reflects the breath of age groups used for targeting. We see FMCG campaigns performing worse because, on balance, they apply a narrower target age range. Realistically, if you’re an FMCG advertiser running a campaign targeting 25-54-year-old females, you are best off benchmarking yourself against other campaigns targeting F25-54, rather than other FMCG campaigns. So, don’t get too hung up on the differences between advertiser category performances; compare against relevant age breaks.

On-target is one thing, delivering target reach is another

Understanding where you’re at against on target benchmarks is important but understanding how your partners deliver target digital reach is really where it’s at.

The DAR benchmarks are a simple way to look at differences in performance. By design, they’re one dimensional in that they look at a single metric i.e. % on-target impressions. They are effective in getting more bang for your buck from your media partners. Digital reach norms are harder to express because they take into account both media volume (impressions/GRPs) and reach delivered, so are best expressed in the form of a classic media reach curve, as in TV.

What is evident from the data is that many publishers have comparative on-target % benchmarks, but huge variance in reach potential. For example, a very active and targeted interest community may be able to deliver exactly the same on-target % as a broad social network with great first party data. However, the broad social network has a reach potential of 80% and the interest community has a maximum reach potential of just 15%.

While this is an extreme example, we see such differences in the ability for partners to provide Reach and Frequency and, if you believe that maximising category buyer reach is a sure-fire way to help your brand grow, then you need to be taking this into account, too.

Viewability vs audiences is not an either/or discussion

There has (rightly) been much focus on measuring viewability in recent times, but often the focus on measuring viewability has come at the detriment of proper digital audience measurement. The reality is that these measures should go hand-in-hand, as both are critical in understanding the digital value equation. Neglecting either measure leaves you enormously exposed to receiving far less value than you expect.

Furthermore, marketers cannot afford to take their eye off long-term brand equity and the important role that digital creative can play in building this. Many brands are still measuring in piecemeal and/or inconsistent ways and simply not unlocking the potential of digital creatives. You cannot lose track of these.

Improving digital campaign accuracy

In conclusion, digital campaigns have much scope for improving accuracy, but there are things you can do. Taking more action in a variety of ways on the insights you’ve got from previous campaigns to improve future results is a must. As is making better use of the available technology as well as incorporating wider sources of data, particularly first party data, into your planning.

Click here to download a copy of the Nielsen Digital Ad Ratings Benchmarks and Findings Report for Europe.

Have an opinion on this article? Please join in the discussion: the GMA is a community of data driven marketers and YOUR opinion counts.

Read also:

How data drives 5 key steps to maximising account-based growth