Open banking has arrived. Recently passed legislation means banks are now opening their data to third parties for the first time. The changes will enable consumers to access their transactional information in ways not previously possible. No-one knows for certain what the implications will be, but there will undoubtedly be interesting and significant changes seen as a result.

The open banking impact, much like GDPR, is raising strategic corporate questions that both banks and the big consultancies are seeking to understand and plan for. Marketers should be doing the same. Consumer behaviour will be affected, so it’s important that brands monitor these developments closely.

While the future is hard to predict, there are several likely outcomes that are worth exploring at this early stage.

Consumer understanding will drive a change in shopping behaviours

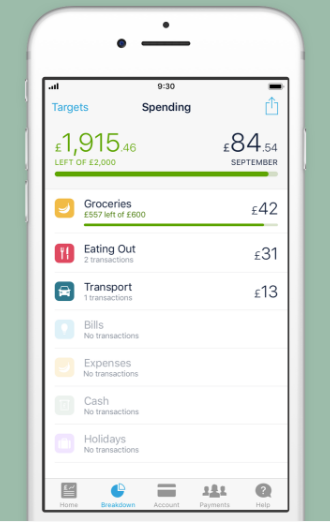

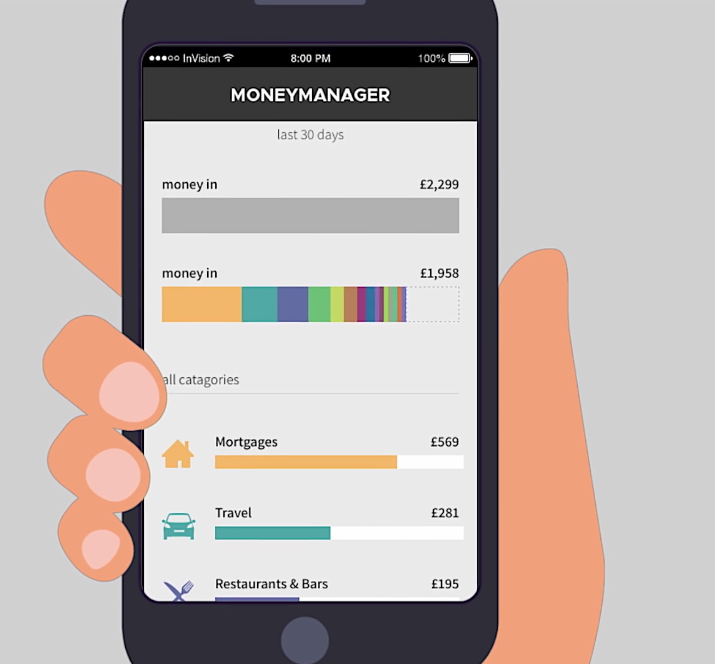

What the fintech disruptors – like Monzo and Revolut – are offering, and what the big banks will now start to replicate, is the opportunity for you to sit back while they take over. They will now collate everything automatically, with no need to trawl through bank statements to see when you last bought a flat white. By simply opening the app, you’ll be met with a clear overview of all your monthly spending. At a glance you’ll know what Deliveroo has been costing you.

Inevitably, this information is going to encourage people to think differently about their spending and some will begin to cut back on non-essentials as a result. Paying for things is getting easier and easier, tapping your card a few times a day or using Apple pay means you can quickly lose track of your outgoings. Open banking will change all that.

Retail needs to get ready, now

The worlds of casual dining and takeaways are likely to be among the first to feel the effects of open banking – mainly because discretionary spending is of course the first to go when people cut back. With the likes of Carluccio’s, Prezzo and Byron reporting struggles recently, casual dining is a sector already in trouble. So, if a negative impact is seen the implications could be serious.

Grocery is another area that might expect to see an immediate impact. Having your grocery shopping detailed in a visual way, alongside the extra shopping you do on top of this, is likely to cause people to re-assess their habitual purchasing behaviour and adjust their approach to the weekly shop. Some of the new purchasing habits that have come to light in recent years, like the top-up shop, might stall or roll back.

Big banks are going to be busy

Clearly, there are ample benefits for consumers. But for banks, there are a number of new challenges to tackle. People will start asking questions they haven’t before, such as: how good is my bank at displaying information to me? Priorities might change and previous issues, such as bank charges, will no longer take centre stage.

A battle of the banks is on the horizon – a giant tech race that is set to disrupt the market. Initially, these services will only suit the tech-savvy consumer, but the easier open banking becomes, the wider take-up will be. Banking apps that aren’t well presented or easy to use won’t last long. Those leading the pack now will need constant updates based on consumer feedback to stay ahead of the game.

What the open banking impact is for marketers

Open banking is only just starting to get off the ground, meaning we can’t yet accurately predict adoption levels. Brands must monitor the landscape and be prepared to implement a plan if they are to be in with a chance of taking the lead. Reacting to changes quickly will be key to success.

Beyond cutting back on take-away coffees and shop-bought sandwiches, it’s the less obvious results that will be the most interesting to observe in the long run. For example, we might see a positive impact on health, as people seek alternatives to jumping in the Prêt queue. Suddenly seeing you’ve been spending £300 a month on lunch is undoubtedly impactful, and healthier choices might well result.

The open banking impact will undoubtedly bring challenges, but there will be opportunities, too. The changes to the retail landscape, alongside the battle of the banks, will affect both consumers and marketers alike. Taking an active interest in the changes now is an essential first step towards being ready to adapt, whatever open banking may bring.

Have an opinion on this article? Please join in the discussion: the GMA is a community of data driven marketers and YOUR opinion counts.